If your Houston home has flooded or if you are just gathering information to make a decision about buying a house, this guide is for you. — whether from Hurricane Harvey, a bayou overflow, a broken pipe, or a slow-motion drainage problem that finally caught up with you — you already know what comes next. The damage is expensive. The repairs are complicated. And selling a flooded house through traditional channels can feel almost impossible.

We have bought dozens of flood-damaged homes across Greater Houston, including in Meyerland, Memorial City, and other neighborhoods that have flooded repeatedly over the years. We know what buyers — including us — look for, what lenders won’t touch, and what your real options are. This guide walks you through everything.

Selling a flooded house in Houston is harder than a normal sale, but it is absolutely doable. Let’s start with what you are actually dealing with.

What Makes a Flooded Home Hard to Sell Conventionally

Most buyers who are financing a home rely on a mortgage lender, and lenders are cautious about flood-damaged properties. Here is why that matters to you as a seller:

- Appraisers must note flood history and visible damage, which directly affects appraised value.

- Lenders often require proof that flood damage has been professionally remediated — not just cosmetically patched.

- If your home is in a Special Flood Hazard Area (SFHA), buyers must purchase flood insurance through the National Flood Insurance Program (NFIP) or a private carrier, which can add hundreds or thousands of dollars per year to their costs.

- Buyers with flood insurance requirements may walk away from deals in high-risk zones entirely.

Even buyers who are not financing can be scared off by uncertainty — especially if they don’t know what’s still hiding in the walls, under the subfloor, or in the crawlspace. Water damage has a way of becoming more expensive the further you dig.

Houston Flood Zones — What You Need to Know Before You Sell

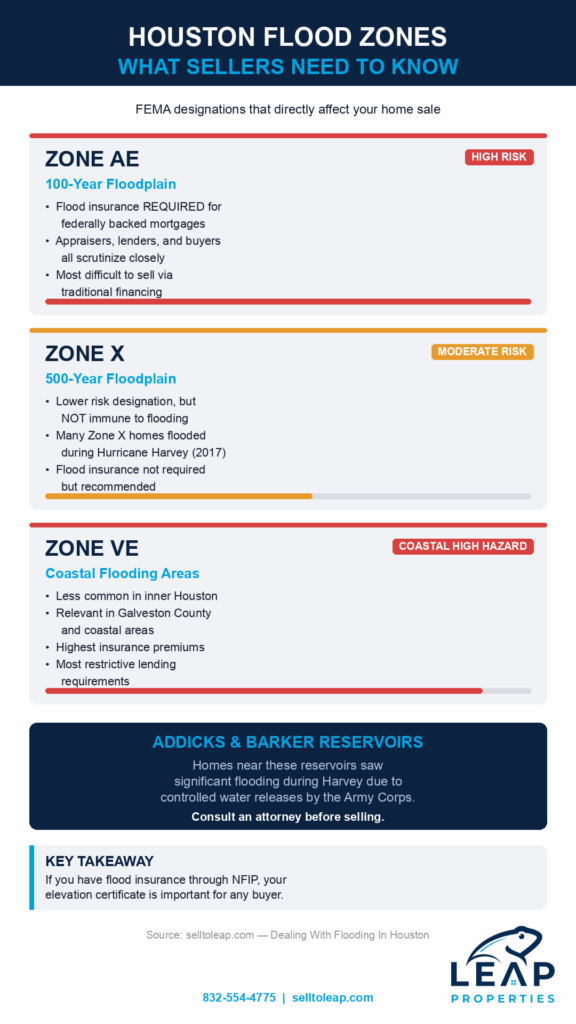

FEMA designates flood zones on Flood Insurance Rate Maps (FIRMs). The Harris County Flood Control District (HCFCD) maintains local flood zone data for Greater Houston, and many neighborhoods have been remapped since Hurricane Harvey hit in 2017. You can use the Harris County Flood Education Mapping Tool to see if you are in a flood zone.

The main flood zone designations that affect home sales:

- Zone AE (100-year floodplain): High risk. Federally backed mortgages require flood insurance. Buyers, appraisers, and lenders will all scrutinize your property closely.

- Zone X (500-year floodplain or moderate risk): Lower risk, but Harvey proved these homes are not immune. Many flooded in 2017 despite being Zone X.

- Zone VE: Coastal high-hazard areas. Less common in inner Houston but relevant in Galveston County areas.

If you have had flood insurance through NFIP, you should have an elevation certificate on file. This document shows your home’s elevation relative to the base flood elevation and is important information for any buyer — and for pricing.

Homes near the Addicks Reservoir and Barker Reservoir saw significant flooding during Harvey due to controlled water releases by the Army Corps of Engineers, which created additional legal complexity for sellers in those areas. If your home is in that zone, consulting an attorney before selling is a good idea.

Texas Disclosure Requirements for Flooded Homes

Texas law requires sellers to disclose known material defects on the Seller’s Disclosure Notice. Flood damage and flood history are material defects — they must be disclosed. Specifically, you are typically required to disclose:

- Whether the property has been damaged by flood, standing water, or drainage problems.

- Whether any part of the property is located in a FEMA-designated flood zone.

- Whether there has been previous water penetration into the foundation, basement, walls, or floors.

Failing to disclose flood history can expose you to legal liability after the sale. Cash buyers who specialize in distressed homes expect flood history and typically won’t hold it against you — but they do need to know the facts so they can price accordingly.

Always disclose fully and honestly. If you are unsure what’s required in your specific situation, consult a Texas real estate attorney.

What Happens to Your Home’s Value After a Flood?

Flood damage affects home value in two ways: the direct cost of damage, and the stigma that remains even after repairs are done.

On the direct damage side, common costs include:

- Drywall and insulation replacement: $3–$10 per square foot depending on scope.

- Flooring replacement: $4–$15 per square foot depending on material.

- HVAC systems: $5,000–$15,000 if water reached major equipment.

- Mold remediation: $1,500–$15,000+ depending on how long moisture was present.

- Structural repairs: Highly variable — can range from minor to six figures in severe cases.

On the stigma side, research consistently shows that homes with disclosed flood history sell for 3–20% less than comparable homes without that history, even after full remediation. In high-flood-risk neighborhoods like Meyerland, that discount can be more pronounced because buyers have more alternatives and more awareness of the risk.

Your Options for Selling a Flooded House in Houston

You have three realistic paths:

1. Repair and list traditionally. If the damage is not too severe and you have the cash or insurance proceeds to fund full remediation, this can get you the highest gross sale price. But repairs take time, cost more than estimates, and a traditional listing still doesn’t guarantee a buyer will qualify for financing on a flood-history home.

2. List as-is on the open market. You can list without repairing and price the home to reflect its condition. You will attract a smaller buyer pool — mostly investors and cash buyers — and you will need to disclose everything. Expect lowball offers and slower time on market.

3. Sell directly to a cash buyer as-is. This is the fastest path. You disclose the damage, we assess the home, and we make an offer based on its as-is value. No repairs, no showings, no contingencies, no lender appraisals. We close on your timeline — typically 7–21 days.

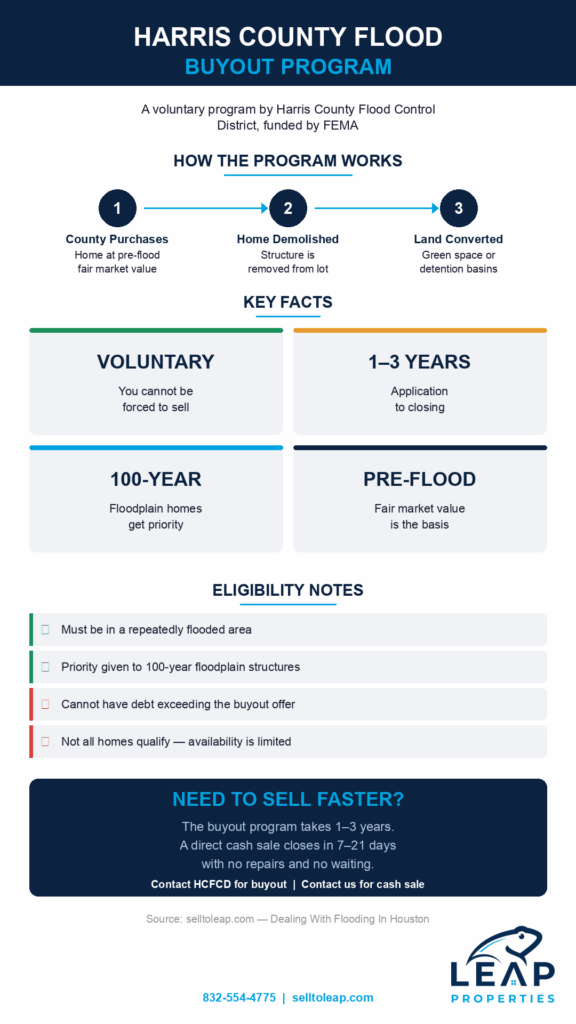

Flood Buyout Programs in Harris County

Harris County has run voluntary flood buyout programs since before Harvey, and the program expanded significantly after 2017. The Harris County Flood Control District, with funding from FEMA, purchases repeatedly flooded homes at pre-flood fair market value, demolishes them, and converts the land to green space or detention basins.

The buyout program is not right for everyone:

- Buyouts are voluntary — you cannot be forced to sell.

- The process is slow — it can take 1–3 years from application to closing.

- Not all homes qualify. Priority is given to structures in the 100-year floodplain that have flooded multiple times.

- You cannot use a buyout if you have significant outstanding debt against the property that exceeds the buyout offer.

If you are interested in the buyout program, contact Harris County Flood Control District directly. If you need to sell faster than the program timeline allows, a direct cash sale is likely a better fit.

Frequently Asked Questions

Do I have to disclose that my house flooded?

Yes. Texas law requires disclosure of known flood damage, flood history, and flood zone status on the Seller’s Disclosure Notice. Failing to disclose can expose you to legal liability.

Can I sell my Houston house if it has mold from flooding?

Yes. Cash buyers who specialize in distressed homes regularly buy properties with mold. You must disclose the mold as a known defect. A traditional listing with active mold is much harder — most lenders won’t finance a home with visible mold damage.

How long does it take to sell a flooded house in Houston?

With a cash buyer, 7–21 days is typical from initial contact to close. A traditional listing with repairs could take 3–6 months or more, depending on the scope of work and buyer financing.

Will my homeowner’s insurance or flood insurance payout reduce my sale price?

If you have received insurance proceeds and have not yet made repairs, a cash buyer will factor in the condition of the home as-is — not the insurance payout. The payout is yours to keep or use toward repairs if you choose to.

What is an elevation certificate and do I need one to sell?

An elevation certificate documents your home’s elevation relative to the base flood elevation. It’s not legally required to sell, but it is helpful information for buyers — especially cash buyers and investors who want to understand flood risk accurately. If you have one, share it.

Does Harvey flood damage still matter in 2025?

Yes. Homes with Harvey flood history are flagged on flood risk databases, and buyers researching a neighborhood will find that history. Disclosure is still required for any known flood damage, regardless of how long ago it occurred.

If you have worked through all of this and decided that repairs, disclosures, and a slow traditional sale are more than you want to take on right now, we can help. We buy flooded homes as-is across Greater Houston — no repairs required, no agent commissions, no uncertainty about financing falling through.

Get A Cash Offer For Your House Today!

Fill Out The Form To Get Started!

Or reach out to us at 832-554-4775!