How to Sell a House with Liens in Texas: The Complete Homeowner’s Guide

Discovering liens on your Texas property when you’re ready to sell can feel like hitting a brick wall. Whether you’re facing foreclosure, relocating for work, or simply ready to move on, liens don’t have to derail your real estate goals. While the process becomes more complex, thousands of Texas homeowners successfully sell properties with liens every year. This comprehensive guide will walk you through everything you need to know to navigate this challenging but manageable situation.

Understanding Property Liens

A lien represents a legal claim against your property that secures payment of a debt or obligation. In Texas, liens are particularly powerful because they “run with the land” – meaning they attach to the property itself rather than just you as the owner. This characteristic means that liens typically must be satisfied before you can transfer clear, marketable title to a buyer.

Understanding how liens work in Texas is crucial because the state follows specific legal procedures that can significantly impact your options and timeline. Texas is what’s known as a “race-notice” state for lien priority, meaning the first lien properly recorded in the public records generally takes priority, with some important exceptions we’ll explore.

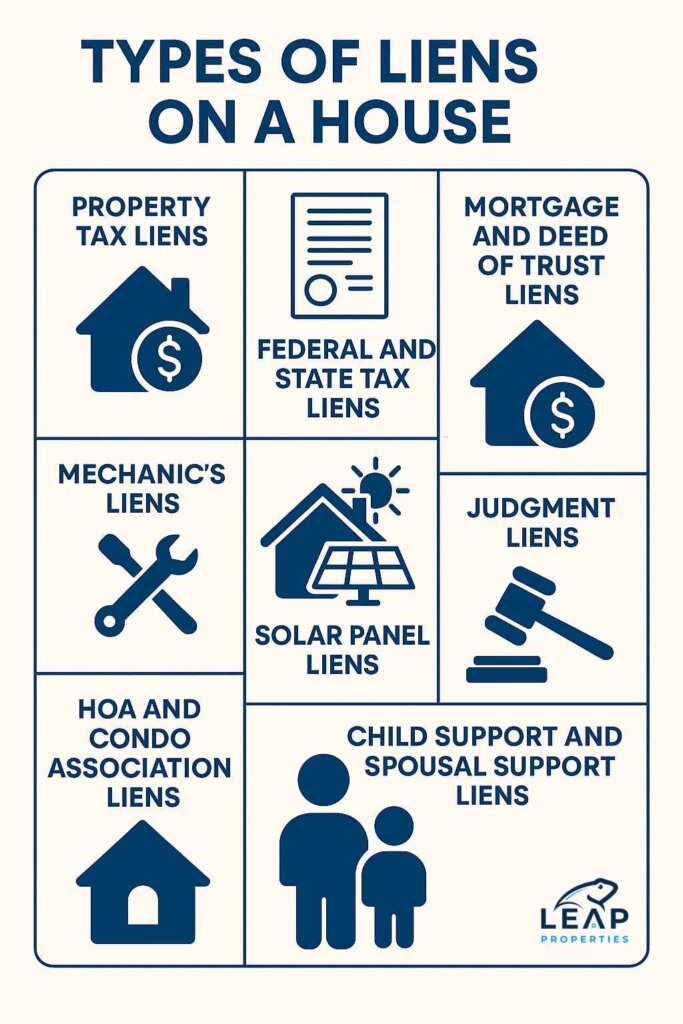

The Complete Spectrum of Liens You Might Encounter

Property Tax Liens: The Priority Giant

Property tax liens hold super-priority status in Texas, meaning they trump virtually all other liens, including mortgages. These liens can include county property taxes, school district taxes, municipal taxes, and special district assessments. What makes property tax liens particularly serious is that Texas allows for tax foreclosure sales where your property can be sold at public auction, often for a fraction of its market value.

Property tax liens accrue interest at rates that can reach 25% annually, plus additional penalties and attorney fees. Even if you’re current on your mortgage, failure to pay property taxes can result in losing your home entirely. The good news is that property taxing authorities are often willing to work with homeowners who are actively trying to sell, sometimes agreeing to accept payment from closing proceeds.

Federal and State Tax Liens: The IRS Factor

When you owe back taxes to the IRS or Texas Comptroller’s office, these agencies can file liens against all your property, including your home. Federal tax liens are particularly problematic because they can attach to property you acquire even after the lien is filed. These liens often carry substantial penalties and interest, and both the IRS and state agencies have extensive collection powers.

However, federal tax liens can sometimes be subordinated or withdrawn if you can demonstrate that doing so will facilitate collection of the tax debt. The IRS also has programs for taxpayers in financial hardship that might provide options for resolving liens with less than full payment.

Mortgage and Deed of Trust Liens: Your Largest Obligation

Your mortgage represents a voluntary lien you agreed to when purchasing or refinancing your home. In Texas, most mortgages are secured by deeds of trust, which give lenders specific powers including non-judicial foreclosure. If you’re behind on payments, your lender may have already begun foreclosure proceedings, which creates additional urgency for resolving the situation through sale.

First mortgages generally take priority over second mortgages, home equity lines of credit, and most other liens (except property taxes). However, if you have multiple mortgages or have refinanced several times, determining exact priority can become complex and may require legal assistance.

Mechanic’s Liens: The Construction Complication

Texas has broad mechanic’s lien laws that allow contractors, subcontractors, suppliers, architects, and even equipment rental companies to file liens against your property for unpaid work or materials. These liens can be filed even if you paid the general contractor but the contractor failed to pay subcontractors or suppliers.

Mechanic’s liens in Texas must be filed within specific timeframes, usually four months from the last work performed or materials supplied. However, the deadline can vary based on the type of work and when preliminary notices were provided. These liens can be particularly tricky because homeowners often don’t learn about them until attempting to sell or refinance.

The key with mechanic’s liens is acting quickly. Texas law provides specific procedures for challenging invalid liens, and waiting too long can limit your options.

Solar Panel Liens: The Modern Challenge

Solar panel liens have become increasingly common in Texas as solar installations have expanded. These liens can take several forms and create unique challenges for home sales.

Solar Loan Liens

Solar Loan Liens occur when you financed your solar panel installation. The financing company may have filed a UCC lien or other security interest against the solar equipment, which can complicate the sale since the panels are now part of your real property.

Solar Lease Liens

Solar Lease Liens arise from leased solar systems. While technically not traditional liens, solar leases create ongoing obligations tied to your property that must be addressed before sale. Some solar lease agreements include clauses that make the remaining lease payments immediately due if the property is sold.

PACE Liens

PACE Liens (Property Assessed Clean Energy) are special assessment liens used to finance solar and other energy-efficient improvements. These liens are particularly problematic because they’re often structured as property tax assessments, giving them super-priority status. PACE liens typically transfer with the property, meaning buyers must assume the ongoing payment obligations.

Power Purchase Agreement Obligations

Power Purchase Agreement Obligations can create situations where your property is encumbered by long-term contracts requiring new owners to purchase power from the solar system at predetermined rates.

Solar liens require special attention because many real estate professionals aren’t familiar with them, and resolution can involve complex negotiations with solar companies, financing entities, and sometimes multiple parties with competing interests.

Judgment Liens: Court-Ordered Obligations

When someone sues you and wins a monetary judgment, they can typically file that judgment as a lien against your real estate in any Texas county where you own property. Judgment liens can arise from various situations: unpaid credit cards, medical bills, business debts, or even court-ordered damages from accidents or disputes.

Texas judgment liens are valid for ten years and can be renewed, making them long-term problems that don’t disappear with time. However, Texas homestead laws provide some protection for your primary residence against judgment liens, except for specific types of debts like taxes, mortgage payments, home equity loans, and improvements to the homestead.

HOA and Condo Association Liens

Homeowners associations and condominium associations in Texas have significant lien rights for unpaid assessments, dues, fines, and legal fees. These liens can accrue substantial interest and attorney fees, sometimes growing much larger than the original debt.

Texas law gives HOAs specific collection powers, including the ability to foreclose on properties for unpaid assessments. However, HOA liens are generally subordinate to first mortgage liens, which can affect collection strategies and your negotiation position.

Child Support and Spousal Support Liens

Texas automatically creates liens against real property for unpaid child support or spousal support obligations. These liens don’t require separate filing and take effect by operation of law. Support liens can be particularly challenging because they involve ongoing court supervision and often require specific court approval for resolution.

IRS and State Employment Tax Liens

If you own a business and have unpaid employment taxes (withholding taxes, Social Security, Medicare), the IRS and Texas Workforce Commission can file liens against your personal property, including your home. These liens are considered trust fund taxes and carry severe penalties, including potential personal liability that survives bankruptcy.

Utility Liens and Special Assessment Liens

Some Texas municipalities and utility providers can file liens for unpaid utility bills, while special districts can create liens for improvements like sidewalks, street lighting, or drainage projects. These liens often carry high interest rates and can be subject to foreclosure proceedings.

The Strategic Approach: Your Step-by-Step Action Plan

Step 1: Comprehensive Lien Discovery and Documentation

Begin with a thorough title examination that goes beyond basic searches. Order a complete title commitment from a reputable title company, but don’t stop there. Check records in every county where you’ve owned property in Texas, as some liens can attach to all your property statewide.

Search federal tax lien records through the IRS, and check for state tax liens with the Texas Comptroller’s office. Review court records for any judgments against you, even in cases where you might not remember the final outcome. Contact your mortgage servicer for exact payoff amounts and any outstanding issues.

For solar installations, gather all original contracts, financing agreements, and correspondence. Contact the solar company and any financing entities to understand exactly what obligations exist and how they’re secured.

Create a comprehensive lien inventory that includes the original amount owed, current balance with interest and fees, the priority level of each lien, and contact information for each lienholder. This inventory becomes your roadmap for resolution.

Step 2: Accurate Property Valuation and Equity Analysis

Understanding your property’s true market value is crucial for developing an effective strategy. In Texas markets that have experienced significant appreciation, you might have more equity than expected, while in areas that have seen declining values, you might face a more challenging situation.

Obtain multiple opinions of value: a comparative market analysis from experienced local real estate agents, a formal appraisal if the situation warrants the expense, and online valuation tools for additional perspective. Consider factors that might affect value such as needed repairs, market conditions, and the time required to sell.

Calculate your net equity by subtracting all lien amounts (including estimated interest and fees through a projected closing date) from your property’s estimated value. Don’t forget to account for selling expenses including real estate commissions, title insurance, attorney fees, and any necessary repairs or improvements.

This analysis determines whether you’re in a position to pay off all liens from sale proceeds (positive equity situation) or whether you’ll need to negotiate with lienholders for reduced settlements (negative equity situation).

Step 3: Lien Priority Analysis and Strategic Planning

Understanding lien priority under Texas law is essential for developing an effective resolution strategy. Property tax liens almost always take first priority, followed by mortgage liens recorded before other liens, then additional liens generally in the order they were recorded.

However, this general rule has exceptions. Some liens can gain priority through specific legal procedures, while others might be subordinate regardless of recording date. Federal tax liens, for example, can be subordinated under certain circumstances, while mechanic’s liens might gain priority over previously recorded mortgages if proper notice procedures were followed.

Your priority analysis should identify which liens must be paid in full versus those where you might have negotiation leverage. Higher-priority lienholders generally have stronger collection positions and less incentive to compromise, while lower-priority lienholders might accept reduced payments rather than risk receiving nothing.

Step 4: Systematic Lienholder Communication and Negotiation

Approach lienholder negotiations strategically rather than randomly. Start by understanding each lienholder’s position and motivations. A mortgage company facing foreclosure has different concerns than a contractor seeking payment for work performed two years ago.

For property tax liens, contact the taxing authority’s collection department early in the process. Many Texas taxing authorities have programs for taxpayers who are actively trying to sell their property and can provide temporary payment deferrals or agreements to accept payment from closing proceeds.

When dealing with federal or state tax liens, explore options like lien subordination, withdrawal, or compromise. The IRS has specific procedures for taxpayers who can demonstrate that lien release will facilitate collection of the tax debt. State tax authorities often have similar programs.

For judgment liens and smaller debts, emphasize the reality of your situation. Explain that you’re selling the property and provide documentation of the property’s value and other liens. Many judgment creditors will accept substantially less than the full amount owed rather than risk receiving nothing if you file bankruptcy or lose the property to foreclosure.

Solar lien negotiations can be particularly complex because they often involve multiple parties. Solar companies may be willing to facilitate transfers to new owners, while financing companies might accept early payoff discounts. PACE liens typically can’t be negotiated away but might be assumable by qualified buyers.

Step 5: Professional Team Assembly and Coordination

Successfully selling a house with liens requires coordinating multiple professionals who understand both Texas real estate law and the specific challenges liens create.

Real Estate Attorney Selection

Choose an attorney who regularly handles real estate transactions involving liens. They should be familiar with Texas lien law, foreclosure procedures, and negotiation strategies. Your attorney can review lien validity, negotiate with lienholders, and ensure all legal requirements are met during resolution.

Ask potential attorneys about their experience with your specific type of liens. Solar liens, for example, require different expertise than traditional judgment liens or tax issues.

Real Estate Agent Expertise

Select an agent who has successfully sold properties with liens and understands how to market such properties effectively. They should be comfortable working with extended timelines and managing buyer expectations throughout the process.

Your agent should understand how liens affect pricing strategy. Properties with liens sometimes need to be priced more aggressively to attract buyers willing to deal with the complexity, while other situations might benefit from higher pricing if equity exists to pay off all liens.

Title Company Capabilities

Choose a title company with specific experience handling complex lien situations. They’ll need to coordinate simultaneous lien payoffs, ensure proper documentation, and manage the intricate closing procedures required when multiple lienholders are involved.

Some title companies specialize in difficult transactions and have established relationships with common lienholders that can facilitate smoother resolutions.

Additional Professional Resources

Depending on your situation, you might need additional expertise. Tax professionals can help with IRS negotiations and tax implications of debt forgiveness. Bankruptcy attorneys might be consulted if your debt situation extends beyond just the house liens. Solar system specialists can help evaluate technical aspects of solar liens and equipment transfers.

Advanced Resolution Strategies for Complex Situations

The Short Sale Alternative When Equity is Insufficient

When your property’s value doesn’t cover all liens, a short sale might be your best option. This process involves getting lienholders to accept less than the full amount owed in exchange for releasing their liens and allowing the sale to proceed.

Short sales require extensive documentation of financial hardship and typically take longer than conventional sales. However, they can be preferable to foreclosure and might preserve more of your credit rating.

Federal Tax Lien Short Sales

The IRS has specific procedures for short sales involving federal tax liens. They might accept less than full payment if you can demonstrate that accepting the reduced amount will result in more collection than pursuing other remedies. This process requires detailed financial disclosure and often involves negotiating with IRS collection specialists.

Multiple Lienholder Short Sales

When multiple liens are involved, coordinating a short sale becomes more complex because each lienholder must agree to accept reduced payment. Success often depends on convincing the first mortgage holder (usually the largest creditor) to agree to terms that leave some proceeds for other lienholders.

Solar Lien Short Sales

Solar liens add unique complexity to short sales because solar companies and financing entities may have different priorities than traditional lenders. Some solar financing agreements include clauses that accelerate all payments upon property sale, while others might allow assumption by qualified buyers.

Lien Subordination and Release Strategies

Federal Tax Lien Subordination

The IRS can subordinate its lien position to facilitate property sales when they determine that subordination will increase the likelihood of tax collection. This process requires demonstrating that the sale proceeds will be used to pay the subordinated IRS lien or that subordination will improve the IRS’s overall collection position.

Mortgage Lien Subordination

In some situations, mortgage lenders might agree to subordinate their position to facilitate resolution of other liens, particularly when they believe it improves their overall collection prospects. This strategy is more common when the mortgage lender is facing foreclosure and recognizes that cooperation might yield better results than proceeding with foreclosure.

Partial Payment and Settlement Negotiations

Judgment Lien Settlements

Judgment creditors often accept substantial discounts from the face value of their judgments, particularly when they understand the alternatives might be receiving nothing. Successful negotiations often involve demonstrating the creditor’s actual collection prospects and offering immediate payment of the reduced amount.

Medical Lien Negotiations

Medical providers and their collection agencies frequently accept reduced payments, especially for older debts. Hospital liens and medical judgments can often be settled for 20-40% of the original amount when you can provide immediate payment.

Contractor and Mechanic’s Lien Settlements

Contractors and suppliers who filed mechanic’s liens are often willing to negotiate, particularly when significant time has passed since the work was completed. They face ongoing legal expenses to enforce their liens and often prefer negotiated settlements to uncertain litigation outcomes.

Texas-Specific Legal Considerations and Protections

Homestead Exemptions and Their Impact

Texas homestead laws provide significant protections for primary residences, but understanding their scope and limitations is crucial when dealing with liens. The homestead exemption protects your primary residence from forced sale to satisfy most types of debts, but important exceptions exist.

Liens That Can Foreclose on Homestead Property

Despite homestead protections, certain liens can still force the sale of your primary residence. These include purchase money mortgages (the loan you used to buy the house), refinance mortgages and home equity loans (if properly executed), property tax liens, mechanic’s liens for improvements to the homestead, and federal tax liens in some circumstances.

Liens That Cannot Foreclose on Homestead Property

General judgment liens, credit card judgments, medical bill judgments, and most other unsecured debt judgments cannot force the sale of your Texas homestead. However, these liens remain attached to the property and must typically be resolved before you can sell with clear title.

Understanding which liens can and cannot foreclose helps prioritize your resolution efforts and negotiation strategies.

Property Tax Foreclosure Procedures

Texas property tax foreclosure procedures are particularly aggressive compared to other states. Taxing authorities can foreclose relatively quickly, and the foreclosure process provides fewer protections than mortgage foreclosure.

Property tax sales in Texas can result in losing your property for a fraction of its value, as properties are often sold for the amount of back taxes owed rather than market value. However, Texas law does provide redemption rights that allow property owners to reclaim their property within specific timeframes by paying the full amount of back taxes, penalties, interest, and costs.

Mechanic’s Lien Procedures and Deadlines

Texas mechanic’s lien law is complex and provides different deadlines and procedures depending on the type of work performed and the parties involved. Residential mechanic’s liens must generally be filed within four months of the last work performed, but the deadline can be extended if proper preliminary notices weren’t provided to property owners.

Understanding these deadlines can be crucial in challenging invalid liens or negotiating with contractors who may have procedural defects in their lien filings.

Solar Lien Legal Considerations

Solar liens in Texas can involve complex interactions between real estate law, secured transaction law (UCC), and contract law. PACE liens are treated as property tax assessments under Texas law, giving them super-priority status and making them particularly difficult to challenge or negotiate.

Solar lease agreements often include specific provisions about property transfers that can create obligations for new property owners. Understanding these provisions is crucial for determining whether solar obligations can be transferred to buyers or must be resolved before sale.

Marketing and Selling Strategies for Lien-Encumbered Properties

Pricing Strategies That Work

Pricing a property with liens requires balancing several competing factors. You need sufficient proceeds to pay off liens while also attracting buyers willing to deal with the complexity and potential delays.

Premium Pricing Strategy

When you have significant equity above your lien obligations, you might price at or above market value, particularly if you’re willing to handle all lien resolution before closing. This approach requires having sufficient liquid funds to pay off liens before closing or the ability to negotiate simultaneous payoffs at closing.

Discount Pricing Strategy

When liens consume most or all of your equity, aggressive pricing might be necessary to attract buyers and facilitate negotiations with lienholders. Buyers who are willing to deal with lien complications might expect discounts in exchange for the additional risk and complexity.

Market-Rate Pricing with Transparency

Some situations allow for market-rate pricing when you can demonstrate a clear plan for lien resolution and work with experienced buyers who understand the process. This approach requires excellent communication and strong professional support.

Marketing Approaches That Attract the Right Buyers

Investor Marketing

Real estate investors often have experience with lien-encumbered properties and may be more willing to proceed with purchases involving liens. Marketing to investor networks, wholesaler groups, and cash buyer networks can expand your potential buyer pool.

Owner-Occupant Considerations

Traditional homebuyers seeking primary residences might be more hesitant about lien complications, but many will proceed if they understand that liens will be resolved before closing. Clear communication about your resolution plan and professional management of the process can help maintain buyer confidence.

Disclosure and Transparency Strategies

Texas law requires disclosure of known material defects and conditions, and while liens are typically discovered during title examination, known liens should be disclosed early in the marketing process. Transparency about liens and your resolution plan builds trust and prevents deals from falling apart when liens are discovered later.

Managing Buyer Expectations Throughout the Process

Timeline Communication

Buyers need to understand that lien resolution can extend closing timelines significantly. Provide realistic estimates and regular updates throughout the process to maintain buyer commitment.

Documentation Sharing

Consider sharing your lien resolution progress with buyers to demonstrate forward movement and maintain confidence in the transaction. This might include copies of settlement agreements, payoff letters, or negotiation correspondence (with sensitive information redacted).

Professional Reassurance

Having experienced professionals manage the process provides reassurance to buyers who might be nervous about lien complications. Your real estate agent, attorney, and title company should be prepared to explain the process and timeline to concerned buyers.

Common Pitfalls and How to Avoid Them

The Hidden Lien Discovery

One of the most devastating problems in lien sales is discovering additional liens after you’ve already committed to a sale price or closing date. This problem occurs when initial title searches are incomplete or when liens are filed in different counties or by different names.

Prevention Strategies

Conduct comprehensive searches that include all variations of your name, check federal and state tax records separately from local title searches, and review all counties where you’ve owned property in Texas. Search business records if you’ve operated businesses, as business liens can sometimes attach to personal property.

Response Strategies

When new liens are discovered late in the process, immediate action is crucial. Contact the lienholder immediately to understand the debt and explore resolution options. Communicate with your buyer and real estate team about the delay and revised timeline. Consider whether the newly discovered lien changes your overall strategy or makes the sale unfeasible.

The Negotiation Breakdown

Lien negotiations can break down for various reasons: unrealistic expectations from lienholders, insufficient time for complex negotiations, or misunderstanding of legal priorities and collection alternatives.

Prevention Through Preparation

Start negotiations early in the process rather than waiting until you have a purchase contract. Understand each lienholder’s legal position and collection alternatives before beginning negotiations. Prepare detailed financial information that demonstrates your situation and the benefits of settlement.

Recovery Strategies

When negotiations stall, consider bringing in professional negotiators or attorneys who specialize in lien resolution. Sometimes a fresh perspective or different approach can break through impasses. Explore alternative resolution strategies like partial payments over time or creative settlement structures.

The Closing Day Crisis

Problems that emerge on closing day can derail months of preparation and negotiation. Common issues include liens that weren’t properly released, last-minute demands from lienholders, or discovery that lien resolution funds are insufficient.

Prevention Through Planning

Coordinate all lien payoffs well before closing day, with confirmed payoff amounts and release procedures. Have contingency funds available for unexpected costs or changes in lien amounts. Work with your title company to prepare detailed closing statements that account for all lien payoffs and associated costs.

Crisis Management

When closing day problems occur, remain calm and focus on solutions rather than blame. Your professional team should have experience handling these situations and can often find ways to resolve issues quickly. Consider whether short-term solutions like escrow agreements or post-closing corrections might solve immediate problems while preserving the overall transaction.

The Tax Consequence Surprise

Debt forgiveness from lien settlements can create unexpected tax obligations. When lienholders accept less than the full amount owed, the forgiven debt might be considered taxable income under federal and state tax law.

Planning Considerations

Consult with tax professionals before finalizing settlement agreements to understand potential tax consequences. Explore whether you might qualify for exceptions like insolvency or qualified principal residence exclusions. Consider the timing of settlements and their impact on your overall tax situation.

Documentation Requirements

Keep detailed records of all settlement agreements and debt forgiveness amounts. Lienholders who forgive more than $600 in debt are required to provide Form 1099-C, but you should maintain your own records regardless.

Conclusion: Moving Forward with Confidence

Selling a house with liens in Texas presents challenges that can seem overwhelming initially, but thousands of homeowners navigate this process successfully every year. The key to success lies in understanding your situation thoroughly, developing a strategic approach, and working with experienced professionals who can guide you through the complexities.

Remember that liens don’t make your property unsellable – they simply add complexity that requires careful management and realistic expectations. Whether you’re facing foreclosure pressure, dealing with unexpected liens, or planning a strategic sale to resolve accumulated debts, the process can be manageable with proper preparation and professional support.

If you are looking for a way to navigate the process without all the hassles – reach out to us. We buy houses with liens.